The Retirement Gap

The difference between the retirement income you’ll need—and what your current plan is positioned to deliver.

Most people are saving something for retirement. The bigger question is whether that savings is structured to produce the income your lifestyle will require—through market cycles, taxes, inflation, and a longer life expectancy. The shortfall between income needed and income expected is what we call the Retirement Gap.

If you’ve never measured your gap, you’re not alone—most retirement plans were built to accumulate, not to distribute efficiently.

Why The Retirement Gap Happens

Retirement gaps usually aren’t caused by “not saving.” They’re caused by assumptions that don’t hold up when retirement turns from a date on the calendar into a 20–30+ year income timeline:

-

Inflation quietly raises the finish line. The cost of everyday living rarely stays flat.

-

Taxes can change the net income you keep. What looks “big” on paper can shrink after taxes.

-

Market volatility creates timing risk. Poor early retirement returns can damage long-term outcomes.

-

Longevity risk is real. Running out of income is a bigger threat than most people expect.

-

Access and flexibility matter. Not all “retirement money” is easy to use when life changes.

The gap isn’t just a number—it’s a planning signal. It tells you what must be structured, protected, and coordinated.

Closing The Gap Requires More Than Just a Bigger Account Balance

Closing the retirement gap isn’t simply “save more.” It’s about building an income strategy that is designed to be predictable, tax-aware, and resilient—so your retirement isn’t dependent on perfect timing or perfect markets.

-

Income First: What will reliably show up each month when work stops?

-

Tax Efficiency: How much of your income will you keep—not just withdraw?

-

Risk Management: How does your income plan hold up during down markets?

-

Flexibility: Can you adapt without disrupting the entire plan?

This is exactly why the Retire pillar exists inside the Fortis Legacy Diamond—because retirement isn’t just accumulation. It’s distribution with control.

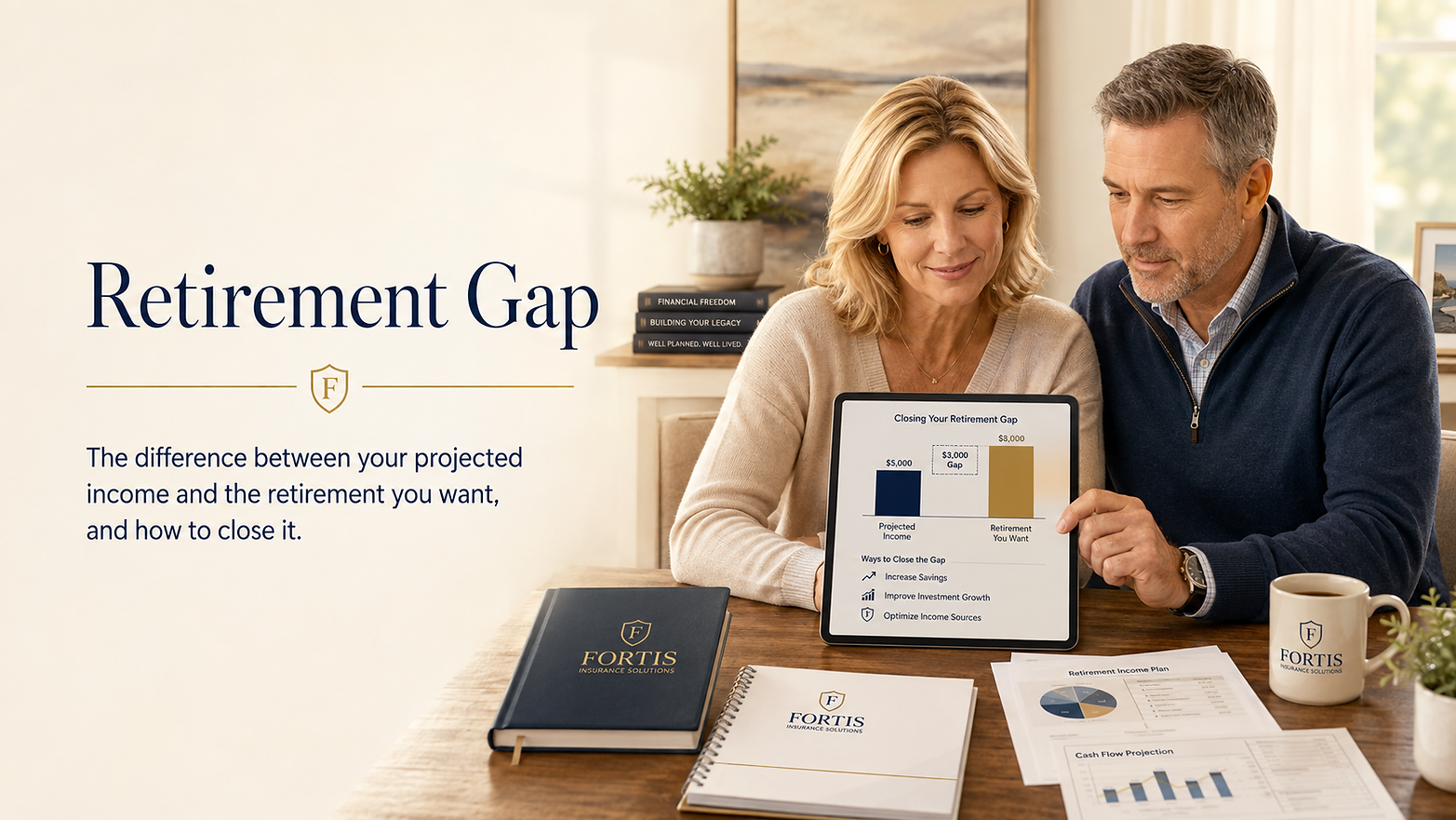

A Simple Retirement Gap Snapshot

Here’s a simple way to think about it:

-

Estimate the monthly income you want in retirement.

-

Identify the reliable income sources you expect (Social Security, pensions, rental income, etc.).

-

Determine the income your assets are positioned to produce (after taxes and market risk).

-

The difference between what you want and what you’re positioned to generate is your Retirement Gap.

Note: A large portfolio does not automatically mean a small gap—because income depends on taxes, volatility, and withdrawal strategy.

Once the gap is visible, the next step is designing a strategy that closes it with structure—not guesswork.

Example: If your desired retirement income is $5,000 per month, but your current strategy is positioned to generate $3,500 per month after taxes and market considerations, the $1,500 difference represents your retirement gap.

How the Fortis Legacy Diamond Helps Address the Retirement Gap

The Fortis Legacy Diamond is built as a coordinated financial system—so your retirement strategy doesn’t operate in isolation. Each pillar supports the others, helping reduce inefficiencies and strengthen your long-term outcome.

When these pillars work together, retirement income becomes more stable, more flexible, and more intentional.

Want to Know Your Retirement Gap?

If you’d like, we can run a simple, confidential retirement-gap review to help you understand:

-

What your current strategy is positioned to generate

-

Where risk or inefficiency may be creating a shortfall

-

What adjustments may help close the gap using a structured approach

Once the gap is clear, the next step is structuring income so retirement isn’t dependent on market timing or tax uncertainty.

Disclosure

Educational content only. Not tax or legal advice. Strategies and outcomes vary based on individual circumstances, product design, and policy/contract terms. Guarantees are backed by the claims-paying ability of the issuing carrier.